Setting the asking price is one of the biggest decisions you’ll make before selling your house.

That’s why some sellers wonder if a pre-listing appraisal is the safest way to price their home.

After all, an appraisal tells you what your home is worth, right?

Not exactly.

A pre-listing appraisal gives you a number on paper.

But that number does not automatically tell you where your list price should land in the current market.

For most sellers, getting a home appraised before selling is unnecessary.

This guide explains why most sellers don’t need one, when it may still make sense, and how it compares to a CMA.

Why most sellers don’t need an appraisal before selling

Here are the three biggest reasons most sellers can skip an appraisal before listing.

The appraised value can skew your list price

One of the biggest risks of getting a pre-listing appraisal is putting too much weight on the appraised value when setting your list price.

You would think an appraisal would make pricing your home easier.

But the price adjustments appraisers make between comparable sales do not always reflect what buyers in your market are actually willing to pay.

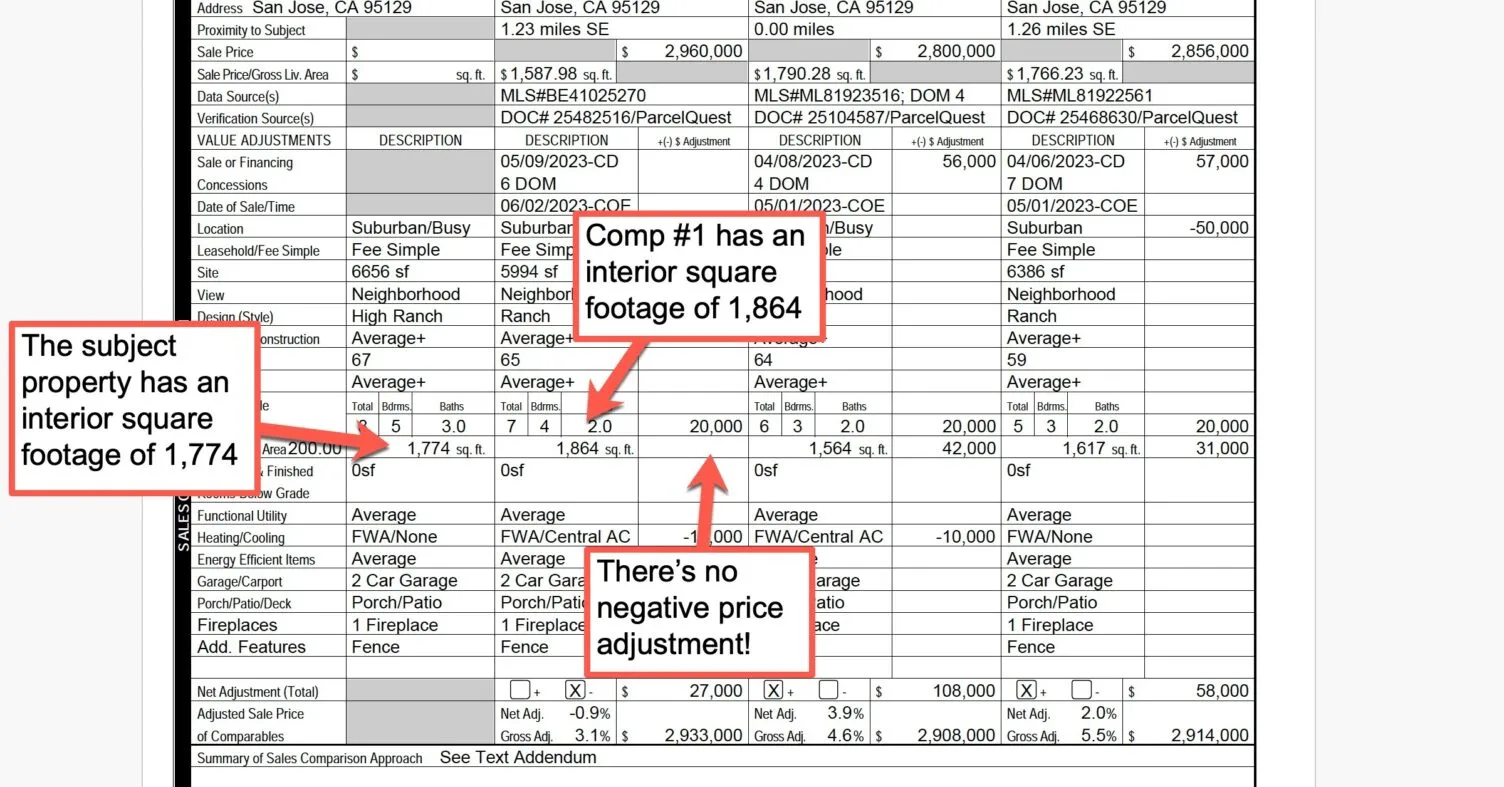

Look at the example in the screenshot below.

You can see that the subject property has 1,774 square feet.

And the first comparable sale has 1,864 square feet.

That’s a 90-square-foot difference.

But where’s the value adjustment?

There isn’t one.

In this case, the appraiser decided that difference did not justify a price adjustment.

A buyer or buyer’s agent may see that very differently.

That’s the problem.

A pricing decision is not just about math.

It’s also about how buyers compare your home to nearby alternatives.

An appraisal can follow a structured process and still miss how the market reacts to certain features or differences between homes.

And when that happens, that number is not the best guide for setting your asking price.

If you rely too heavily on that number, you could list too high, list too low, or price your home in a way that does not reflect current buyer behavior.

The better question is not just what one appraiser thinks your home is worth.

It’s how your home stacks up against competing listings and recent comparable sales in your market.

It can make price negotiations harder

Getting too attached to the appraised value can weaken your negotiating position.

Here’s why.

Let’s say you decide to get an appraisal and the value comes in at $500,000.

To be cautious, you set your asking price at $475,000.

A buyer offers $460,000.

You still have $500,000 in your head, so countering at $470,000 feels reasonable.

But the buyer sees it differently.

They believe their offer already reflects the condition of your home and nearby comparable sales.

So they walk away because the gap feels too wide.

Now you’ve lost a serious buyer and increased your days on market.

That can cause the next offer to come in even lower because buyers may start to think they have more negotiating leverage.

That doesn’t mean the appraisal was useless.

It means the appraised value can become a mental anchor that makes it harder to respond to real buyer feedback.

A pre-listing appraisal is an extra cost

According to the National Association of Realtors, a typical home appraisal costs $500.

That’s one more expense to add before your home even hits the market.

That money could be better spent on things that bring more value when getting your house ready to sell.

For example, you could put it toward minor repairs, paint touch-ups, curb appeal, or other updates that make your home show better to buyers.

You could also put that money toward a seller’s home inspection, moving costs, or other selling expenses.

Here’s the point.

For most sellers, the cost of an appraisal is better spent elsewhere.

You’re usually better off putting that money toward improvements, prep work, or selling expenses that can more directly support your listing.

When a pre-listing appraisal may make sense

While most sellers don’t need one, there are a few situations where getting an appraisal before selling may make sense.

The property was inherited

Getting an appraisal before selling an inherited house makes sense if you need to help establish the home’s fair market value for tax or estate purposes.

It can also help in more practical situations.

For example, you may live out of the area and not know the local market well.

Or multiple beneficiaries may disagree about what the property is worth.

In those cases, an independent appraisal can give everyone a neutral opinion of value.

That can help the people involved decide whether to list, keep, or buy out another share.

You’re going through a divorce

Having your home appraised before listing can also make sense if you’re selling because of a divorce.

This is especially true if the two spouses do not agree on the home’s value, the list price, or which real estate agent to hire.

Having a neutral opinion of value can help reduce disputes over pricing so the sale can move forward more cleanly.

It can also help if one spouse decides to keep the home instead of selling it.

In that case, the appraisal can help support buyout discussions and reduce disputes over what the property is worth.

The home has unique features

Some homes are harder to price because there are not enough comparable sales that truly match them.

That can happen when a home has:

- A large non-rural lot

- Waterfront views

- An ADU

- Features that are uncommon in the local market.

In that situation, getting an appraisal can help give you a more objective starting point.

It will not tell you the perfect list price.

But an appraisal is more useful when your home does not line up cleanly with nearby comps and pricing is less straightforward.

What an appraisal is mainly used for in a home sale

An appraisal is mainly used in the sale of a home when the buyer is getting a mortgage.

The home serves as collateral for the loan, so the buyer’s lender wants to confirm the property is worth enough to support the purchase price.

That’s why the lender typically orders an appraisal after a purchase agreement is signed.

The appraiser evaluates the home using a formal process based on comparable sales, property features, and current market data.

An appraisal relies on a more formal sales-comparison approach, and lender standards generally require at least three closed comparable sales.

How an appraiser determines the value is the same whether the appraisal is ordered by a lender or a seller.

But the purpose is different.

In a financed sale, the appraisal helps the lender confirm the property is worth what the buyer is paying for it.

A seller who gets an appraisal before listing their home is looking for an independent opinion of value.

Those are two different goals.

The lender is trying to confirm collateral value for the loan.

The seller is trying to decide how to price the home before it hits the market.

Appraisal vs. CMA: Which is better before listing?

An appraisal is not the only way to estimate your home’s value before it hits the market.

A comparative market analysis, or CMA, can also help you evaluate what your home could be worth.

A CMA can factor in homes that recently sold, homes already under contract, and homes currently competing for buyers.

Both use comparable sales and a review of the property to estimate value.

But they’re not trying to answer the exact same question.

An appraisal mainly helps the lender decide whether the property is worth enough to support the purchase price.

A CMA helps estimate what price a buyer may realistically pay for the home in the current market.

The biggest difference is the formal valuation rules the appraiser has to work within.

Appraisers have to abide by specific requirements when making price adjustments between the subject property and comparable sales.

Plus, they use a more conventional sales-comparison approach.

A CMA does not follow those same formal standards.

That gives a real estate agent more flexibility when adjusting for the value of key features and characteristics.

For example, in a higher-priced market, central AC may carry more weight with buyers than an appraiser’s adjustment reflects.

The same can happen with an awkward layout.

An appraiser may not make much of a downward adjustment for it.

But a good agent knows that an undesirable floor plan can have a real impact on buyer demand.

So they can factor that into the CMA when recommending a list price.

That doesn’t just affect the price.

It also affects how quickly the home draws showings and whether buyers feel urgency.

That’s why a CMA from the right agent is usually more useful before selling.

Not because an appraisal is wrong.

Because a CMA helps you estimate what buyers may actually pay and how you should position your home in the market.

Here’s a quick look at the key differences between an appraisal and a CMA.

| Appraisal | CMA | |

| Cost | $400–$800 | Free |

| Timeline | 1–4 weeks depending volume of appraisals | 1–3 days |

| Responsible party | Appraiser | Realtor |

| Point of view | Rigid industry parameters | Potential buyers’ priorities |

The bottom line on getting an appraisal before selling

One of the biggest fears sellers have is pricing their home wrong before it hits the market.

You may think the safest way to avoid that mistake is to get an appraisal before you put your house on the market.

But for most sellers, it is not the best way to land on the right list price.

What helps more is knowing where your price needs to land to attract buyers without leaving room for the market to turn against you.

And working with the right real estate agent from the start can help you make that decision with more confidence.