Most buyers and sellers prioritize the price when buying or selling a home.

Is the sale price important?

Absolutely.

But one aspect people often overlook is the contingency clauses in a real estate contract.

Contingencies are the number one reason for the sale of a home falling through after the seller has accepted the buyer’s offer.

The problem?

Many people get engaged in the selling or home buying process –– without being aware of how these provisions can impact their home sale.

But my goal is to help you navigate around that obstacle.

This guide will tell you everything you need to know about real estate contingencies.

Here’s what you’ll learn:

- The definition of a contingent listing

- Why contingencies are important in a real estate deal

- Common contingencies

- How a contingent offer works

- Tips to navigate the contingency process.

Let’s dive in.

What does contingent mean in real estate?

Contingent means being conditional upon specific circumstances.

In real estate, a contingent listing indicates that although an offer has been accepted by the seller, the final sale is dependent upon specific conditions, such as the home’s value matching or exceeding the sale price according to the buyer’s appraisal.

This contingent status means the property is in a state of limbo, awaiting the fulfillment of any contract conditions.

You’ll see “contingent” on a house for sale after the seller’s real estate agent changes the status from “active” in their local MLS.

This typically happens shortly after the seller and the buyer have ratified the purchase agreement.

During this contingent phase, both parties work diligently to satisfy any conditions.

This period can involve activities such as conducting a home inspection, the buyer securing financing, negotiating repairs, and more.

It’s a critical time when both sides collaborate to ensure all prerequisites are met to move forward.

So when you see a house that is “contingent,” it simply means that the sale of the home is under contract but includes one or more stipulations that need to be satisfied before the sale can be final.

Why contingencies are crucial in a real estate transaction

A contingent real estate contract is vital for both the buyer and the seller.

Here’s why…

A contingency allows the buyer to back out of the sale of a home (for that contingency reason) and get their earnest money deposit back.

But that easy exit is forfeited once the buyer releases their contingencies.

For example, let’s say a buyer and seller have a ratified contract that is contingent upon a 10-day inspection from the buyer.

The 10-day window gives the buyer the opportunity to cancel the agreement –– without losing their earnest money.

But…

Once the buyer releases their contingencies, then their initial deposit is at risk should they want to back out of the sale (more on this below).

Contingencies are crucial for buyers because they safeguard their earnest money deposit.

Similarly, the removal of these contingencies marks a significant milestone for sellers during the home selling process.

Common real estate contingencies

A buyer’s offer can include different types of contingencies.

These can vary based on:

- Local market conditions

- Advice from their real estate agent

- Unique circumstances and personal preferences.

These factors can shape a buyer’s strategy and influence which contingencies are ultimately included in their offer.

Which conditions are most prevalent?

Here are the most common contingencies that you’re likely to encounter in a real estate transaction.

Inspection contingency

What’s the first thing you think of when you hear “inspection contingency?”

A home inspection contingency?

If so, you would be partially right.

A home inspection is a general inspection of a property.

But an inspection contingency allows a buyer to conduct more than just a home inspection.

This contingency period allows them to have the property inspected for any reason.

Some of the most common property inspections buyers have done include:

- Termite

- Roof

- Pool

- Chimney

- Foundation.

An inspection clause also allows buyers to conduct any and all due diligence on the property that they want.

This is why, in many states, this conditional provision is referenced as an “investigation of property” in the purchase contract.

Here’s an example of that:

Maybe a buyer is thinking of remodeling and wants to bring a contractor out to the house.

Or maybe the home has previous structural modifications and they want to check on the permits.

No matter what it is, this is the time for the buyer to finish doing their homework on the property.

Appraisal contingency

Mortgage lenders require most buyers to get an appraisal when purchasing a home.

Why?

Because the house is being used as collateral for the buyer’s loan.

So lenders want to make sure that the home is worth what the buyer is paying for it.

In many cases, the appraised value will match the sale price (or be very close to it).

This is because an appraiser is aware of the sale price before visiting the property.

But sometimes the appraised value will come in at less than the agreed-upon purchase price.

When this happens, the lender will use the appraised value (and not the sale price) as the number they’ll lend on.

This means the buyer will need to increase their down payment should they want to move forward with the sale.

But an appraisal contingency protects buyers in these scenarios by giving them two other options:

- Back out of the sale (and get their deposit back)

- Renegotiate the price with the seller.

Financing contingency

Many buyers will get pre-approved for a new mortgage before making an offer on a home.

A pre-approval letter from a reputable lender/loan officer is a good start to the loan process.

But it doesn’t guarantee the buyer’s loan.

A financing contingency, also known as a mortgage contingency, is a clause in the purchase agreement that provides a safety net to ensure the buyer can get approved for their new mortgage loan.

The loan process is initiated by the buyer’s loan officer as soon as the property is under contract.

Part of this is submitting the buyer’s documentation to underwriting for a conditional loan approval.

The chances of a strong homebuyer not being fully approved by an underwriter are low.

Which is why buyers who are well-qualified will usually place less importance on a mortgage contingency than buyers who aren’t as confident.

Home sale contingency

When a buyer needs to sell their property before they’re able to purchase a new one, they’ll make an offer contingent upon the sale of their house.

This condition is known as a home sale contingency.

Offers that are contingent on the sale of a home are less desirable to home sellers.

Why?

Because there’s a major hurdle to cross.

The buyer needs to secure a new homeowner for their residence before they can move forward.

However, there are two different scenarios a buyer can be in when making an offer on a house contingent on selling.

And one is more appealing to a home seller than the other.

Both of these situations are commonly referred to as a “home sale contingency.”

But in some states, these sale contingencies are referenced as two different terms.

Sale and settlement contingency

A sale and settlement contingency means the buyer is making the sale contingent upon them receiving an offer on their current residence.

This means that their house is either:

- Not yet listed on the market

- Put up for sale but hasn’t received an offer.

It can take a long time for a real estate transaction to close with this type of stipulation.

Which is why it’s risky for a seller to accept this contingency clause.

And why most sellers who do accept an offer with this provision will do so because their home has been on the market for some time.

Settlement contingency

A settlement contingency means the buyer has a ratified purchase contract on the house they’re selling, but the sale has not yet closed.

This contingency protects the buyer in case the sale of their current home falls through.

A buyer’s offer that includes a settlement contingency presents a risk to a seller –– but the soon-to-be settlement date on the buyer’s home sale drastically lowers that risk.

Title contingency

A title contingency can ensure that the property’s title is clear of any liens, disputes, or legal issues that could obstruct the transfer of ownership.

Some prospective buyers will have access to a preliminary title report before making an offer (provided up front by the seller).

The information the report details about the property includes:

- Legal owners

- Easements and encumbrances

- Mortgage liens

- Tax liens

- Mechanic’s lien (from contractor)

- Unresolved legal claims.

But not all buyers see a title report up front.

And sometimes the report will be outdated or have missing information.

A title contingency gives the buyer the opportunity to investigate the title of the property and verify that the seller can legitimately sell it.

HOA contingency

A buyer who is purchasing a property with a homeowners association (HOA) is required to acknowledge their acceptance of the HOA’s legal documents.

These forms are usually several hundred pages and include things such as the HOA’s:

- Fees

- Restrictions (rentals, pets, etc.)

- Potential future assessments

- Financial statements

- Governing documents (bylaws, CC&R’s, insurance master policy, etc.).

An HOA contingency allows the buyer to review and approve the rules, regulations, and financial health of the HOA before finalizing the purchase.

It protects buyers from unexpected obligations and ensures they are comfortable with the community’s rules and financial status.

How a contingent offer works

A contingent offer is a legal agreement from a homebuyer to purchase a property subject to specific conditions that must be met for the transaction to proceed.

The contingencies specified in the proposed real estate contract only become binding if accepted by the seller.

Here’s how the process of a contingent offer works.

1. The buyer determines which contingencies to include in the offer

A homebuyer has two choices when making an offer on a house:

- Submit a contingent offer

- Submit a non-contingent offer.

When opting to make their offer contingent, the buyer needs to determine which contingencies will be included.

This is the time when most buyers will strategize with their real estate agent.

However, it’s not just about which contingencies to include in the offer.

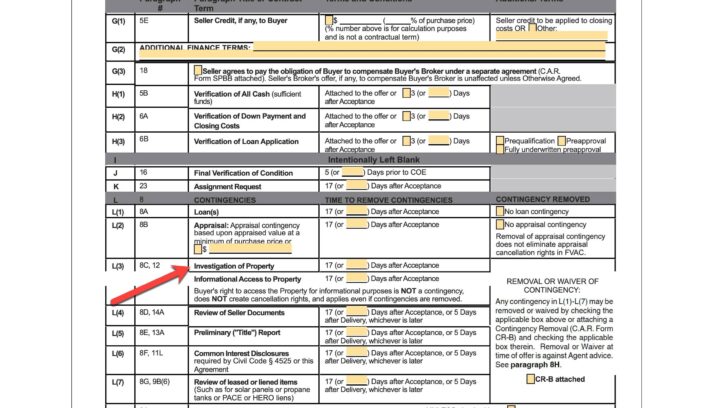

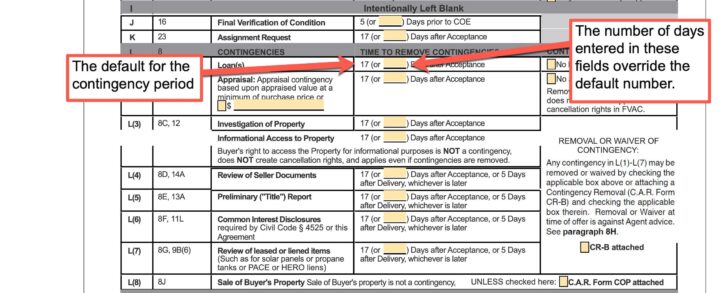

They also need to include the number of days they have to satisfy that contingency.

Most states have real estate contracts that include a default for the number of days for each condition.

But they also have an empty field that can override the default number.

For example, let’s say a buyer wants to make an offer contingent on an inspection of the property.

The offer contract in their state defaults to 17 days for an inspection contingency, but they want to make their offer look slightly better to the seller –– so they adjust the contingent period to 10 days.

Here’s what that looks like:

After determining the contingent terms, the buyer and their realtor will finalize the purchase contract.

The buyer’s agent then submits the offer to the listing agent.

2. The buyer and the seller agree on a contingent contract

Similar to how a buyer has the option of determining contingent terms in their offer, a seller has their own options.

They can respond to the buyer’s contingent offer in one of three different ways:

- Accept

- Reject

- Counteroffer.

The contingency and its time period are negotiable.

So if a seller counters a contingency in a buyer’s offer, it will be for one of two reasons:

- To remove the contingency

- To reduce the contingent period.

The buyer’s act of good faith happens after the contingent offer is agreed to in writing by both parties.

This is done by making their earnest money deposit to the escrow company.

The deposit amount is typically 1-3% of the sale price and made within 1-3 days after the offer has been accepted (negotiable terms and varies by area).

And that initial deposit is why contingencies in real estate are important.

Because the buyer risks losing it to the seller should they want to back out of the sale after releasing them.

This is one reason why understanding how a contingent offer works is included in our list of tips for home sellers.

3. The contingencies must be removed by the deadline date

A contingency date is the deadline specified in the purchase contract by which the buyer must waive the specified condition.

The time period is specific to each individual contingency rather than being collective when multiple contingencies are involved.

Let’s run through a scenario…

A seller accepted a buyer’s offer that included a 10-day inspection contingency and a 14-day appraisal contingency.

The buyer does their due diligence on the property and is comfortable removing the inspection contingency on the 10th day.

This acceptance needs to be stated in writing –– so their agent has them sign a contingency removal form and sends it to the listing agent.

But…

The 14th day comes along, and the appraisal report isn’t completed.

It’s the listing agent’s responsibility to follow up with the buyer’s agent to determine what the buyer wants to do.

The listing agent discusses with the seller and tells them they have two options:

- Extend the contingency period

- Send the buyer a “Notice to Perform.”

If they pick option two, the “Notice to Perform” will be sent to the buyer’s agent and will state the timeframe in which the buyer has to release the contingency.

If the buyer doesn’t?

Then the contract can be canceled by the seller and the listing goes back on the market.

Tips for negotiating real estate contingencies

Navigating contingencies in real estate requires both strategy and insight.

Here are three things to keep in mind to help you negotiate contingencies effectively.

1. Consider the number of days

Timing is everything when it comes to real estate contingencies.

For buyers, a shorter time frame can make an offer more attractive to a seller.

But ensure you give yourself enough time to conduct thorough inspections and secure financing.

Finding the perfect balance is key — too short, and you might rush and miss important details; too long, and the deal might lose its appeal.

What if you’re selling a house?

Be open to the contingency period, but be smart about it.

Does a buyer really need 17 days to conduct due diligence on your property?

A lengthy contingency period can mean a buyer isn’t that serious.

Striking the right balance in the number of days allotted for contingencies can make the difference between a deal that falters and one that flows seamlessly toward closing.

2. Make sure you understand the opt-out clause

Understanding the opt-out clause in a contingency is crucial for both buyers and sellers.

For buyers, it’s your safety net, allowing you to withdraw from the deal without penalty if certain conditions aren’t met.

The key phrase in that last sentence is “certain conditions.”

Because you can only opt out of a home sale (and get your deposit back) for that contingency reason.

Meaning…

Don’t expect to get your earnest money refunded if you want to cancel because you have cold feet.

Make sure you know how you’re protected before writing a contingent offer.

Knowing the limits of a contingency’s flexibility is also key when selling a home.

It helps you prepare for a dreaded situation where a buyer wants to cancel the agreement without penalty.

3. Factor in local market conditions

Contingent offers are more common in a buyer’s market.

Why?

Because house hunters have more leverage in a slower real estate market.

But it’s the opposite when the supply of homes for sale is low and demand is high.

The leverage swings to homeowners.

This is why non-contingent offers are more common in a seller’s market.

You should understand your local market conditions before submitting or receiving an offer on a home.

The right insights can guide your approach.

For example…

You’ll put yourself at a major disadvantage if you write a contingent offer on a home in a hot market.

That’s not to say you shouldn’t…

But you’ll be competing against much stronger offers.

And you’ll increase the chances of having to put your listing back on the market if you’re selling and accept a contingent offer in a market where it’s likely you’ll have multiple offers.

Have your real estate agent educate you about the market conditions in your area so you can adapt your approach accordingly.

The bottom line

Contingencies in real estate can have a big impact on a home sale.

The price is almost always most important to both the buyer and seller, but contingencies come in a close second.

This is why knowing how to find a good realtor is key.

The best ones know the intricacies of every contingency and how to negotiate them favorably for their clients.

FAQs about real estate contingencies

Here are several of the more common questions buyers and sellers have about contingencies in real estate.

Can a seller accept another offer while contingent?

Yes, a seller can accept another offer while their property is under a contingent status, but typically this is subject to certain conditions being met by the initial buyer. Without a “kick-out clause,” the seller may have limited flexibility, yet they can still entertain backup offers. If the initial buyer fails to satisfy the contingencies within the agreed timeframe, the seller may then proceed with a new offer, ensuring the sale process continues smoothly.

What’s the difference between contingent and pending?

A contingent status means a home sale depends on specific conditions being met, such as a buyer obtaining approval for financing. Pending status means all contingencies have been satisfied, and the sale is moving toward closing. Essentially, contingent deals still face hurdles, while pending sales are on a clearer path to closing.

What does no contingencies mean?

A non-contingent offer means that the buyer did not include any contingencies in their offer on a house. This is a sign of a serious buyer because no contingencies means the buyer is risking losing their earnest money deposit should they want to back out of the sale after the purchase contract is ratified.

What is a 10-day contingency in real estate?

A 10-day contingency refers to a condition set in a purchase agreement that must be met within 10 days. Commonly used for inspections of the home, it allows buyers to assess the property’s condition and negotiate repairs or back out of the deal based on the findings within this timeframe.